Quarterly Fund review – March 2022

In this extract from our March 2022 Quarterly Commentary, Julian Morrison, CFA, Investment Specialist, reviews the performance of the Allan Gray Australia Funds. Click here to read the full Quarterly Commentary.

Allan Gray Australia Equity Fund

The Australian sharemarket rose during the March quarter, with the S&P/ASX 300 Accumulation Index returning 2.1%. The Allan Gray Australia Equity Fund outperformed strongly, returning 13.7% during the same period, outperforming its S&P/ASX 300 Accumulation Index benchmark by 11.6%.

The Australian sharemarket rose during the March quarter, with the S&P/ASX 300 Accumulation Index returning 2.1%. The Allan Gray Australia Equity Fund outperformed strongly, returning 13.7% during the same period, outperforming its S&P/ASX 300 Accumulation Index benchmark by 11.6%.

It was a particularly strong quarter for the Equity Fund, during a particularly volatile period for the market, demonstrating the diversification benefits of a contrarian investment approach.

During the quarter, positioning in the Energy sector was the largest positive contributor, followed by some stock-specific holdings in the Materials sector. Within these, Woodside, Santos, Sims, Incitec Pivot, Nufarm, Alumina and South32 were leading contributors. Origin Energy also contributed strongly, although it is officially categorised within the Utilities sector.

Despite recent strong performance, we believe many of these names remain attractively valued versus the broader market, and so we retain meaningful positions. We have, however, trimmed some of these holdings over the quarter, to ensure position sizes remain appropriate.

Holdings within Financials contributed positively overall to performance, although performance at stock level was mixed. NAB has performed strongly for some time, and we lightened exposure quite significantly during the quarter, shifting some of the proceeds into Westpac, which has been much weaker over the last year and we believe offers better value. We added to insurer QBE during a period of notable weakness and subsequently the share recovered to end the quarter positively. Other financial holdings include Challenger and AMP, where our positioning remained largely unchanged.

We have generally avoided Healthcare companies in recent years given excessive valuations. This has benefited relative performance for some time now. However, during the quarter, our most significant addition was to Ansell which sits within the Healthcare sector. Ansell has been an outlier in terms of its underperformance, and we believe it offers much better value than the market at the recently depressed share price. As always, our holdings are decided based on bottom-up company valuation, and our thesis for Ansell is covered in an earlier section of this Quarterly Commentary.

Elsewhere, the absence of exposure to Information Technology companies aided relative performance, as that sector underperformed meaningfully for the quarter. Despite some of these coming off their highs recently, we still do not own any IT stocks. As a general comment, valuations for many of these companies still seem very lofty by our assessment. The IT sector makes up 4% of the Australian market today. This is a similar size to each of the Energy, Consumer Staples and Communication Services sectors. It is noteworthy that the IT sector has quadrupled from 1% of the market five years ago. This is one marker, albeit a simple one, of how extreme the share price growth has been in the sector, some of which may be unsustainable.

The recent shift in market leadership across stocks and sectors seems notable over a three-month period. However, the prevailing trend of the last few years has been so extreme, that this is a relatively small correction in the context of a longer timeframe. Therefore, there has not been a dramatic change in where we see the most value. We continue to manage to appropriate position sizes – generally trimming positions on strength and adding when weaker prices present value. Our investment team maintains a continuous research agenda for new ideas – and those which offer the best value may just make it into the portfolio.

In short, we continually invest your Equity Fund’s assets where we see the best long-term value. The aim is also to avoid investing in companies we see as overvalued and at risk of destroying capital. The gap between these categories remains large, in our view, and continues to present a great opportunity for long term outperformance.

Allan Gray Australia Balanced Fund

The Allan Gray Australia Balanced Fund returned 7.0% for the quarter, outperforming its composite benchmark by 11.3%. This positive performance came during a falling market overall – the composite benchmark fell 4.3% during the quarter.

The allocation to shares contributed positively to absolute performance. Stock selection in both Australian and global shares were the primary contributors to the Fund’s outperformance for the quarter.

The Fund had about 70% asset allocation to shares on average during the quarter. This is after accounting for about 8% of the global share exposure being reduced through the use of exchange-traded derivatives, which allows for some protection in those periods where market indices fall. This positioning also added positively to returns during the period, as markets were generally weak for much of the quarter.

During the quarter, the Fund also held around 18% in fixed income securities and a 4% exposure to gold through an exchange-traded fund. The fixed income allocation has remained significantly shorter in duration than the benchmark – at around two years versus more than seven years for the benchmark.

This means that the fixed income portion of the Fund remains more defensively positioned than the benchmark (in terms of both relative and absolute returns), in the event interest rates rise from current historically low levels. Longer-term interest rates did indeed rise markedly during the last quarter. Therefore, this positioning again contributed positively to relative performance.

As with the Equity Fund, we believe potential portfolio value relative to the market is significant and we continue to manage for risk with a long-term, valuation-driven perspective.

Allan Gray Australia Stable Fund

The Allan Gray Australia Stable Fund returned 4.4% for the quarter, meaningfully outperforming its cash rate benchmark – which effectively returned zero for the quarter.

The Fund had been gradually lightening its ASX-listed securities (primarily equities) exposure for some time leading into the last quarter, as the market had continued to rise. This held the Fund in good stead during a volatile last quarter. Nevertheless, the selected securities held performed well overall and contributed to the strong outperformance. Even with this strong outperformance, we continue to manage exposures to what we believe is a prudent level.

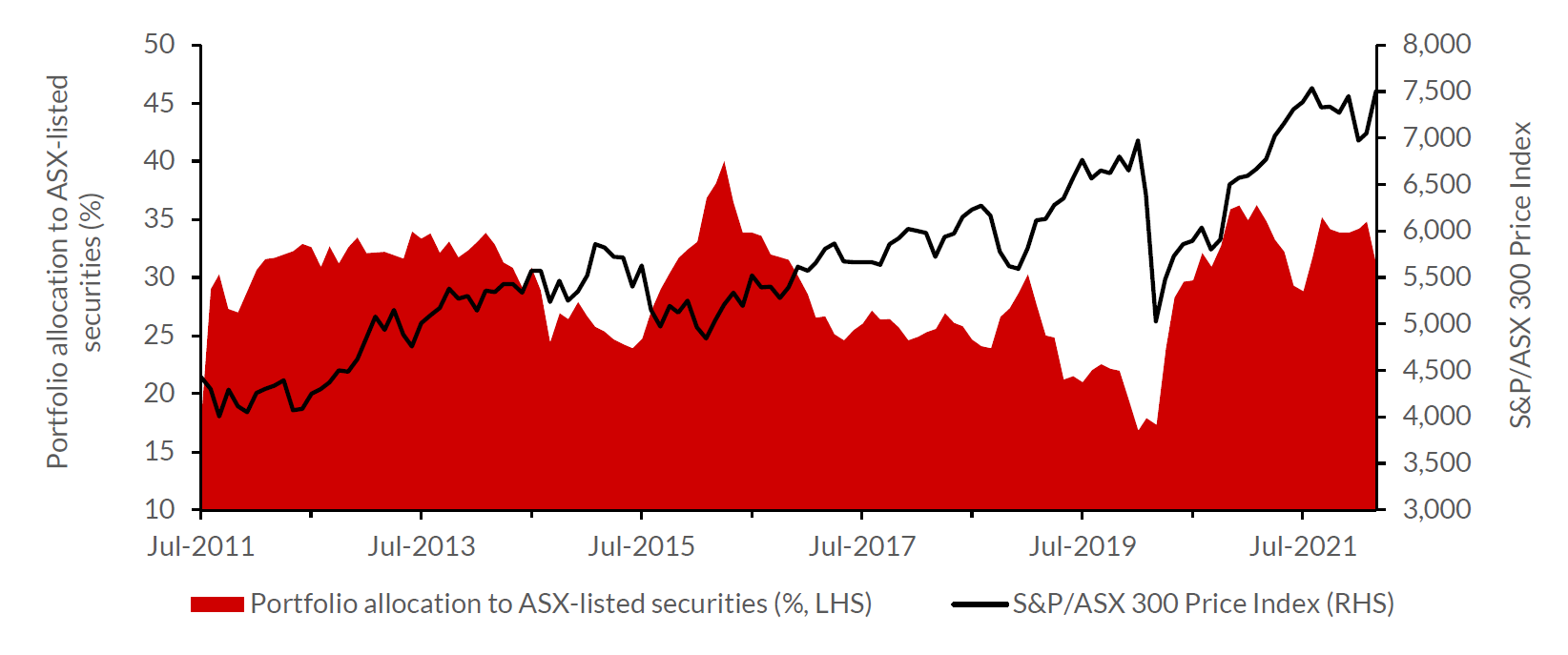

As at the end of March, the Fund had around 31% invested in ASX-listed securities (of which around 28.5% was equities and about 2.6% selected hybrid securities). The remaining 69% is held in cash and money market investments. This can be seen in Graph 1, which shows our allocation between cash and ASX-listed securities over time.

Graph 1: Stable Fund listed security weighting – allocation rises where we see value in listed securities

Source: Allan Gray, Bloomberg, as at 31 March 2022.

The Stable Fund aims to add value from both our disciplined stock selection, and from the decision on how much to allocate to securities versus cash. This provides the Fund with great flexibility to manage risk throughout the market cycle, while still seeking to add long-term returns above cash. We believe the current environment provides a great opportunity for the Stable Fund to demonstrate its intended benefits. It offers a low to moderate risk/return profile, with the potential to outperform cash, while having the advantage of simplicity and ease of understanding.

Julian Morrison holds a Bachelor of Arts (Honours – University of Sheffield) and the Chartered Financial Analyst designation.