Interview with JD de Lange by Zilla Efrat

Interview with JD de Lange by Zilla Efrat

The saying “you get what you pay for” seems to apply to most things in life, but not to active fund manager fees.

JD de Lange, Chief Operating Officer at Allan Gray Australia, says: “Active fund manager services are very different to anything else you are likely to buy. The fees, or price you pay, are transparent: a percentage of the fund’s value. But you don’t really see what you get for the fee. The value is not obvious at all.

“In life, cheaper products are often inferior to expensive ones. But investing is not like that; it’s not like buying a car, for example, with tangible features. If you compare the features of an expensive car with a cheaper one, it’s often easy to see why it costs more.

“When investing in funds, that isn’t necessarily true; it can be very hard to establish value. With active fund managers, you get a promise of performance in exchange for a fee. An expensive product can actually be the weakest product on the market. And the cheapest may perform really well.

“In investing, cheap doesn’t necessarily mean inferior and higher fees don’t produce certainty.”

Do your homework

The damage of poor performance and unnecessarily high fund manager fees can, of course, make a huge difference to one’s retirement savings over the long term.

What’s an investor supposed to do?

“Their homework,” according to de Lange, “and unfortunately there is no shortcut.

“It is not that difficult to find active fund managers who could outperform the market, providing you do your research well, and especially if you look at the longer term. If they have outperformed consistently over, say, five, seven and ten years, the likelihood that they will outperform the market in future becomes higher, assuming their investment approach remains consistent.”

History may not repeat, but it rhymes

Passive or index fund managers sell the message that around 75 per cent of active funds underperform the market and Allan Gray agrees with this.

But de Lange notes that if you buy the market through an index fund, the only thing you can be sure of is that you will get the return of the market, minus the fee for the passive manager. “But if you buy an active manager, you are buying its people, process and philosophy. The result of these three things working together makes up the product,” he says.

“These three features can be replicated in future. The longer they stay in place, the higher the probability of outperformance from the active manager, but of course there’s no certainty. You have to think long term.

“Still, there are quite a few active fund managers in Australia who have outperformed the market over the long term. To outperform, they must be doing something differently. Their style and philosophy must be working. And they must be sticking to it.”

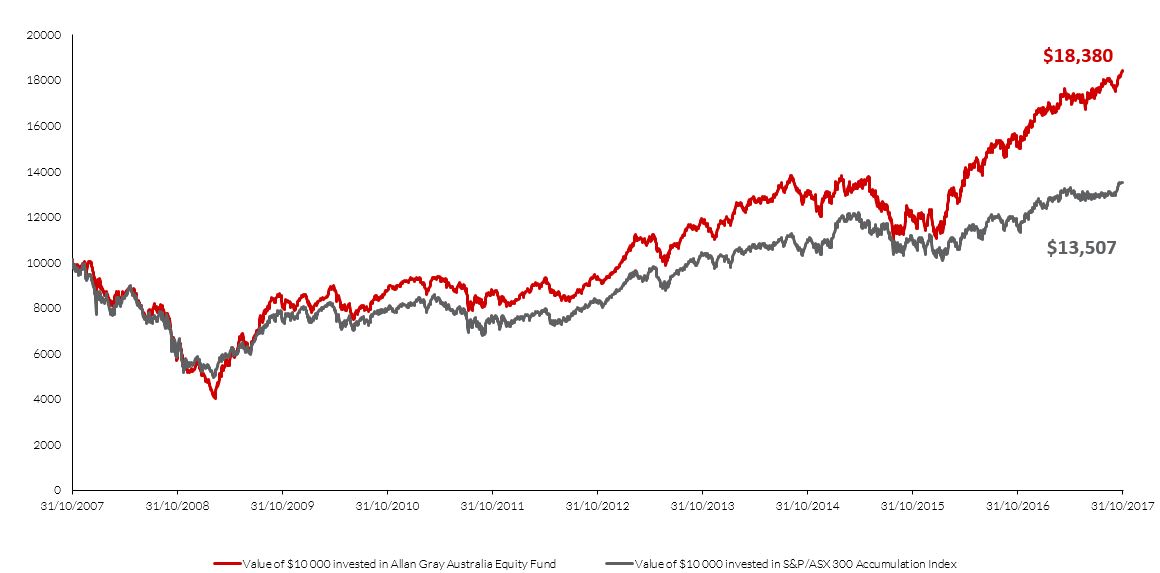

The proof is always in the pudding

De Lange says Allan Gray Australia’s Equity Fund has outperformed the market by more than three per cent after fees each year for 10 years. This may not sound like much, but as the chart shows it made a material difference to wealth over the period due to compounding.

“A poor manager will destroy a lot of wealth regardless of fees. Fees are just the cost of doing business with that manager. They do not indicate value for money in any shape or form. Low fees doesn’t mean better value and you shouldn’t be put off by high fees, so long as the return is commensurate.”

Value of $10,000 invested in the Allan Gray Australia Equity Fund over the last 10 years compared to the index

*Source: Allan Gray Australia, 31 October 20017 to 31 October 2017. Based on a $10,000 initial investment in Allan Gray Australia Equity Fund Class A units. Returns net of fees and assume reinvestment of distributions. Past performance is not a reliable indicator of future performance.

Aligning interests is key

When doing your homework, de Lange says you should also examine whether the manager charges performance-based fees.

“We believe performance-based fees align the interest of the manager with that of the investor. This structure means that we do well when our investors do well. There’s lots of debate around this, but we are confident this structure makes us much more aligned with performance and delivering for clients than merely growing assets.

“There’s currently a perception in Australia that low cost, or low fees, is good in financial services. We think the conversation should be about value for money, not cost. You can’t expect the world if you’re not prepared to pay for it.”

This is a fantastic article and applies to all investors.